Electric Car Depreciation: The EVs Losing the Most Value in 2026

Electric cars can be cheaper to run, but some are losing tens of thousands of pounds in value within just a few years. Our latest study reveals the EVs depreciating fastest.

Electric cars can be brilliant. They’re quiet, quick, cheaper to run for many drivers, and packed with clever tech. But there’s one cost that can sneak up on buyers faster than a rapid charger bill: depreciation.

Electric car depreciation is the amount an EV loses in value over time, usually measured by comparing its current market value against its original purchase price or RRP.

And, according to new Insureworks research, electric car depreciation is becoming one of the biggest hidden costs for EV buyers, with some popular models losing tens of thousands of pounds in value within just a few years.

We analysed a sample of UK used electric vehicle listings and compared average used prices against the original RRP of popular EVs. The study looked at 2025, 2024 and 2023 models listed on Auto Trader to estimate how much value these cars had lost after one, two and three years on the road.

To understand which models are being hit hardest by electric car depreciation, we compared original RRPs against current UK used market prices for popular EVs.

The results? Some EVs are dropping in value seriously quickly.

What did the study find?

Polestar came out as the worst-performing EV brand overall in our analysis.

The Polestar 2 lost an average of 62.1% of its original value after three years. In cash terms, that works out as an average loss of £27,932.

That’s not just a small dip. That’s a huge chunk of the car’s original value gone in the space of three years.

The data also showed that depreciation can hit early. After just one year, the Polestar 2 had already lost an average of 39.6% of its value, equal to an average cash loss of £17,919.

That makes it one of the clearest examples in our research of how quickly electric car depreciation can affect buyers, especially those purchasing new or nearly-new EVs.

Volkswagen, Kia, Tesla and Hyundai also ranked among the fastest-depreciating EV brands in the study, with three-year-old model groups losing more than 55% of their original value on average.

The EVs losing the most value after one year

After one year, Polestar topped the table, followed closely by Volkswagen and Hyundai.

The five electric cars losing the most value after one year were:

| Rank | EV brand / models analysed | Average depreciation | Average cash loss |

| 1 | Polestar / Polestar 2 | 39.6% | £17,919 |

| 2 | Volkswagen / ID.3 and ID.4 | 38.4% | £15,660 |

| 3 | Hyundai / Kona Electric and Ioniq 5 | 35.1% | £14,309 |

| 4 | Kia / Niro EV and EV6 | 34.5% | £15,213 |

| 5 | Audi / Q4 e-tron | 30.4% | £16,271 |

That means some nearly-new EV owners could already be looking at a five-figure drop in value after just 12 months.

The EVs losing the most value after two years

By year two, the losses became even sharper.

| Rank | EV brand / models analysed | Average depreciation | Average cash loss |

| 1 | Polestar / Polestar 2 | 49.8% | £22,496 |

| 2 | BMW / i4 | 45.1% | £24,108 |

| 3 | Volkswagen / ID.3 and ID.4 | 44.5% | £18,125 |

| 4 | Kia / Niro EV and EV6 | 42.9% | £18,492 |

| 5 | Hyundai / Kona Electric and Ioniq 5 | 42.2% | £17,138 |

The BMW i4 is a good example of why it’s worth looking beyond percentages. Its average depreciation rate after two years was 45.1%, slightly higher than Volkswagen at 44.5%, and because of its higher original price, the average cash loss was also larger at £24,108.

In plain English: a lower percentage doesn’t always mean a smaller financial hit.

The EVs losing the most value after three years

After three years, Polestar remained at the top of the depreciation table.

| Rank | EV brand / models analysed | Average depreciation | Average cash loss |

| 1 | Polestar / Polestar 2 | 62.1% | £27,932 |

| 2 | Volkswagen / ID.3 and ID.4 | 58.8% | £24,535 |

| 3 | Kia / Niro EV and EV6 | 56.6% | £24,877 |

| 4 | Tesla / Model 3 and Model Y | 56% | £29,074 |

| 5 | Hyundai / Kona Electric and Ioniq 5 | 55.2% | £23,610 |

By this point, every model group in the top five had lost more than half of its original value on average.

That’s a big deal for anyone planning to sell, part-exchange, refinance or replace their car after a few years.

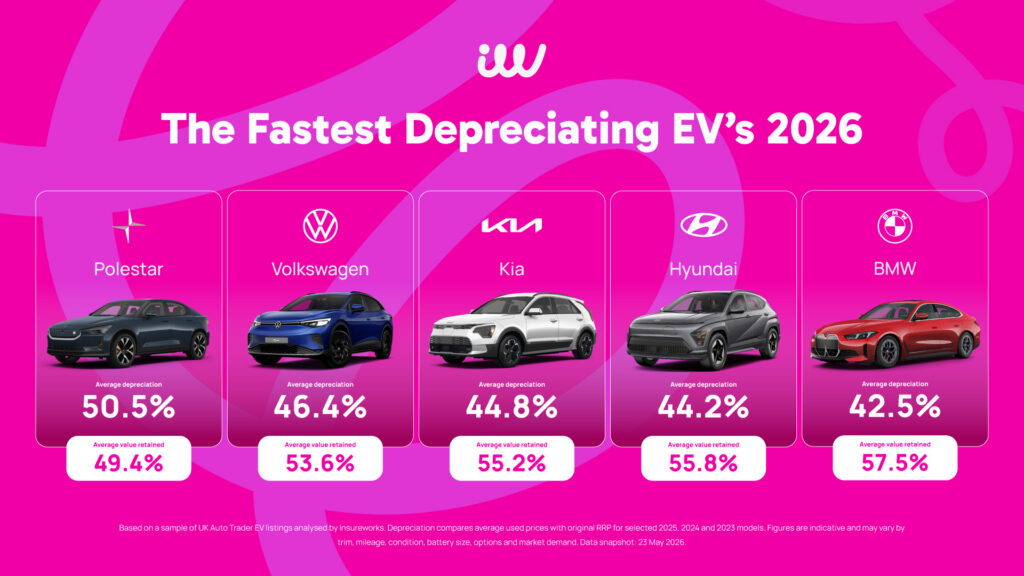

Which EV brands lost the most value overall?

Across all model years analysed, these were the five EV brands with the highest average depreciation:

| Rank | Brand | Average depreciation | Average value retained |

| 1 | Polestar | 50.5% | 49.5% |

| 2 | Volkswagen | 46.4% | 53.6% |

| 3 | Kia | 44.8% | 55.2% |

| 4 | Hyundai | 44.2% | 55.8% |

| 5 | BMW | 42.5% | 57.5% |

Polestar had the highest average depreciation overall, while Volkswagen, Kia and Hyundai also saw sharp value drops across the models analysed.

At the other end of the table, Volvo performed strongly in our dataset. The Volvo EX30 lost an average of 32.7% across the available one and two-year data, making it the strongest value-retainer overall in the study.

Tesla also performed better in the early stages. Across the Model 3 and Model Y, Tesla models lost just 8.9% on average after one year. However, depreciation accelerated by year three, with three-year-old Tesla models losing an average of 56.0% of their original value.

Why are some EVs depreciating so quickly?

There isn’t just one reason. EV values can be affected by a mix of factors, including:

- high original purchase prices

- changing battery technology

- increased supply of used electric cars

- new model discounts

- uncertainty around battery health

- changing demand in the second-hand market

- finance and leasing stock entering the used market

EV technology is moving quickly. Newer models often bring better range, faster charging and updated features, which can make older models feel less attractive to used car buyers.

That doesn’t mean these cars are bad. Far from it. Many used EVs can offer excellent value, especially when someone else has taken the biggest depreciation hit.

But for new and nearly-new buyers, depreciation is something worth understanding before signing on the dotted line.

Why depreciation matters if your car is written off or stolen

Here’s where things get important.

If your car is written off or stolen, your standard motor insurer will usually pay out based on the car’s market value at the time of the claim.

Not what you originally paid.

Not necessarily what you still owe on finance.

And not always enough to replace the car with a brand-new equivalent.

So, if your EV has dropped sharply in value, there could be a shortfall between your motor insurance payout and the amount you need to clear finance or replace the vehicle.

That shortfall is the “gap” GAP insurance is designed to help with.

A simple example

Let’s say you buy a new EV for £45,000.

A couple of years later, it’s written off, and its market value has dropped to £25,000.

Your motor insurer may base its payout on that £25,000 market value. But if you still owe more than that on finance, or you want to get back to the original invoice price, you could be left out of pocket.

That’s where GAP insurance can help provide extra protection, depending on the type of policy you choose and the policy terms.

No crystal ball. No complicated waffle. Just cover designed to help with the financial shortfall if the worst happens.

What does this mean for EV buyers?

For used EV buyers, this level of depreciation could be good news. A nearly-new electric car may offer much better value than buying brand new, especially if a large chunk of depreciation has already happened.

For new EV buyers, it’s worth thinking about the full cost of ownership. That means looking beyond the monthly finance payment, charging costs and road tax. Depreciation can be one of the biggest costs of owning a car, even if you don’t feel it until you come to sell or change vehicle.

Before buying a new or nearly-new EV, it’s worth asking:

- How quickly has this model been losing value?

- Am I buying outright, on finance or through a lease?

- What would happen if the car was written off?

- Would my motor insurance payout be enough?

- Could I afford the shortfall if there was one?

Not the most exciting questions, we know. But they could save you a serious headache later.

EVs can still make loads of sense for drivers. Lower running costs, home charging, smooth driving and strong performance all make electric cars appealing.

But our research shows that depreciation can be steep, especially for certain brands and models.

The key is not to panic. It’s to understand the numbers before you buy.

If you’re purchasing a new or nearly-new EV, GAP insurance could help protect you from a potential shortfall if your car is written off or stolen while it’s still losing value quickly.

At Insureworks, we keep things simple. No faff. No confusing jargon. Just straightforward cover that helps you understand what protection actually makes sense for you.

Insureworks analysed a sample of UK used electric vehicle listings and compared average used prices against original RRP to calculate estimated depreciation.

The dataset focused on popular electric car brands and models, including Tesla Model 3, Tesla Model Y, Audi Q4 e-tron, BMW i4, Kia Niro EV, Kia EV6, Volvo EX30, Volkswagen ID.3, Volkswagen ID.4, Hyundai Kona Electric, Hyundai Ioniq 5 and Polestar 2.

Disclaimer: This analysis is based on a sample of UK used electric vehicle listings reviewed by Insureworks. Average used prices were compared against original RRP figures to estimate depreciation across selected 2025, 2024 and 2023 EV models. Used prices can vary depending on mileage, specification, trim, battery size, condition, location, optional extras, dealer pricing and market demand.

The figures should be treated as indicative market estimates rather than guaranteed resale values or vehicle valuations. Rankings only include models where there was sufficient source data available in the dataset. Data snapshot: 21 May 2026.

Insureworks Ltd (Firm Reference Number: 1040384) is an appointed representative of Your Company Matters Limited (Firm Reference Number: 486123) which is authorised and regulated by the Financial Conduct Authority (FCA)